The private sector contributed ₹33,979 crore (22.56%) to India’s total defence production of ₹1,50,590 crore in FY 2024-25, the highest-ever participation since 2016-17.

Defence Production in India

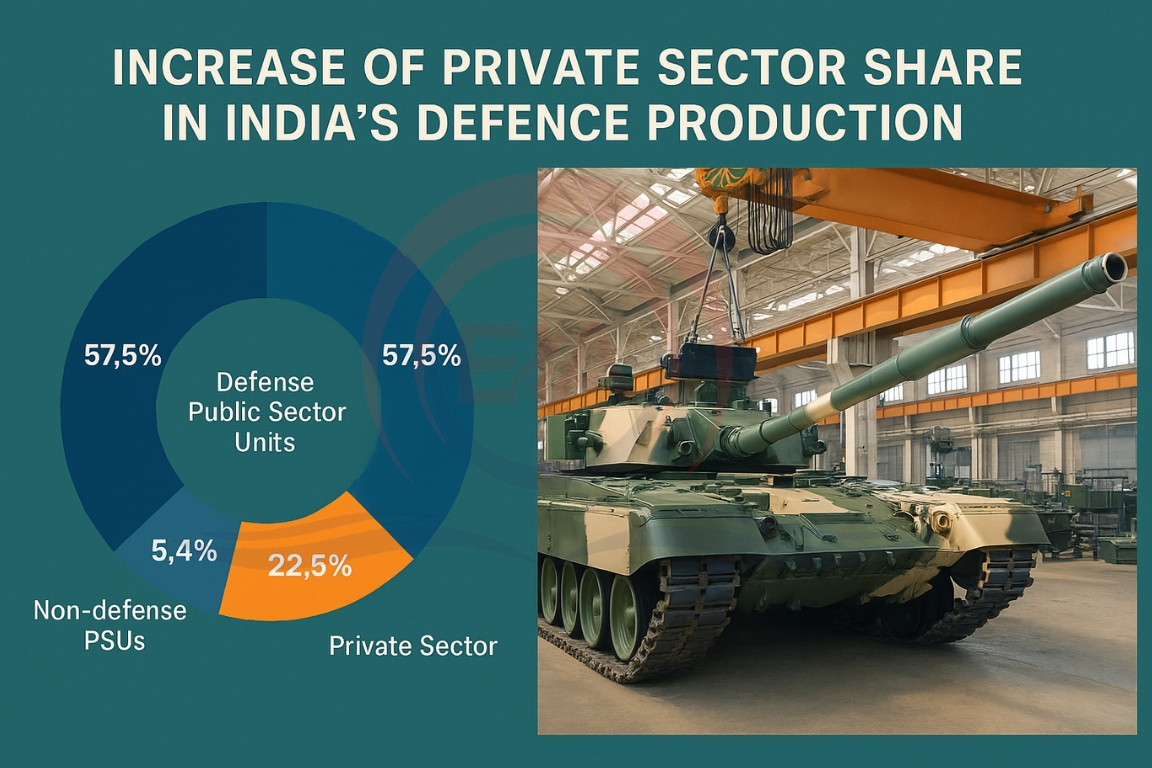

Sectoral Share (FY 2024-25):

- Defence Public Sector Units (DPSUs) → 57.50%

- Ordnance Factories → 14.49%

- Non-defence PSUs → 5.4%

- Private Sector → 22.56%

Defence Budget Expansion:

- Grew from ₹2.53 lakh crore (2013-14) to ₹6.81 lakh crore (2025-26).

Production Milestones:

- Defence output touched a record ₹1.50 lakh crore (2024-25), more than 3 times the 2014-15 level.

- 65% of defence equipment is now indigenously manufactured (earlier import dependence was 65–70%).

- Target: ₹3 lakh crore by 2029 to establish India as a global hub.

Growth in Defence Exports

- Exports grew 34-fold, from ₹686 crore (2013-14) to ₹23,622 crore (2024-25).

- Exported items include bulletproof jackets, helicopters, interceptor boats, lightweight torpedoes.

- India exports to 100+ countries; U.S., France, Armenia were top buyers in 2023-24.

Government Interventions

- Innovation & R&D

- iDEX (Innovations for Defence Excellence): Encourages startups in defence tech.

- ADITI scheme (₹750 crore, 2023–26): Focuses on critical tech like AI, quantum, nuclear, space, and underwater surveillance.

- DTIS: Improves testing facilities for the aerospace & defence sector.

- Industrial Corridors: Defence Industrial Corridors in Uttar Pradesh & Tamil Nadu promote local manufacturing with incentives.

- Indigenisation Push: SRIJAN (2020): Lists imported items for domestic manufacturing to reduce dependency.

- Ease of Doing Business: Defence Product List simplified (2019). Licence validity extended from 3 years to 15 years, with further extension up to 18 years.

Way Forward

- Level Playing Field: Transparent procurement to ensure fair competition between private firms and DPSUs.

- Strengthen Export Base: Expand destinations, support private firms in global markets.

- Boost Startups: Widen iDEX and ADITI coverage for emerging defence domains (AI, cyber, quantum).

- Joint Ventures: Partner with global defence majors for co-development & technology transfer.

- Skill Development: Training programmes for advanced defence technologies to create a specialised workforce.

Conclusion:

India’s growing private sector role in defence reflects a shift towards self-reliance and global competitiveness. Sustained reforms, innovation, and partnerships will be crucial for achieving the ₹3 lakh crore production target by 2029.