The Centre has proposed major reforms in the Goods and Services Tax (GST) structure by removing the 12% and 28% slabs. The plan aims to simplify the tax system, ease the burden on consumers, and boost compliance.

Goods and Services Tax (GST)

- GST is a single indirect tax system introduced to replace multiple central and state taxes like excise duty, service tax, VAT, etc.

- It was launched in India on 1st July 2017.

- It is a destination-based tax (collected at the place of consumption, not origin).

- It is levied on the supply of goods and services, with exceptions such as alcohol (for human consumption), petroleum products (currently outside GST), and electricity.

- Over time, concerns arose about its complexity, revenue leakages, and inverted duty structures.

Key Features of the Proposal

- The government is now pushing for “next-generation GST reforms” to make the system more efficient.

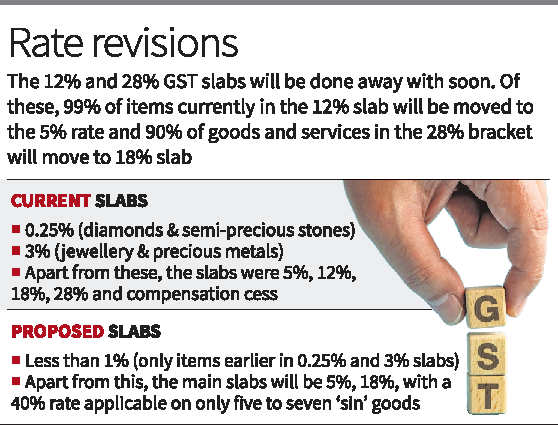

- Removal of 12% and 28% Slabs: Goods in the 12% category will mostly move to the 5% rate. Nearly 90% of items in the 28% slab will shift to 18%.

- Introduction of Two Special Rates: Ultra-low rate (<1%) for precious metals like gold, silver, and semi-precious stones. High “sin rate” (40%) only for 5–7 harmful products such as tobacco and gutka.

- No Additional Cess: Cess charges will not be added over the GST rates.

Revenue Implications

- 28% slab contributes ~11% of GST revenue, while 12% gives ~5%.

- Majority of revenue (~67%) already comes from the 18% slab.

- Government expects short-term revenue dip but hopes higher consumption and better compliance will compensate.

Impact on Consumers and Industry

- Lower tax on aspirational goods such as air conditioners and appliances.

- Everyday items like toothpaste, soap, and shampoo could become cheaper.

- Uniform tax rates on similar products (e.g., all savouries taxed alike).

Other Reform Measures

- Ease of Living: Faster registration, pre-filled returns, and quicker refunds using technology.

- Fixing Inverted Duty Structure: Aligning input and output tax rates to prevent working capital blockages for businesses.

GST – CONSTITUTIONAL AMENDMENT

- The Constitution (One Hundred and First) Amendment Act, 2016 enabled the introduction of GST in India.

- Key provisions:

- Inserted Article 246A – gives both Parliament and State Legislatures power to make laws on GST.

- Inserted Article 269A – provides for levy and collection of IGST on inter-state trade, which is shared between Centre and States.

- Inserted Article 279A – provides for the creation of the GST Council (Union Finance Minister + State Finance Ministers) to recommend tax rates, exemptions, model laws, etc.

- Amended Seventh Schedule – subsumed many taxes of Union and States under GST.

Conclusion:

The proposed GST reforms aim to simplify the tax system, reduce consumer burden, and widen the tax base. While there may be an initial fall in revenue, increased consumption and better compliance are expected to balance it out, making the GST framework more transparent and growth-friendly.